Why haven't interest rate increases been effective?

As we roll around to another expected interest rate increase and discussions inevitably turn to mortgage repayments and household spending, the nuances of demographics are often lost in the debate. As is the impact on the Australian dollar and businesses that employ our workforce. The focus is always residential mortgages and how much it will add to monthly repayments. That’s about as detailed as it usually gets.

So why haven’t interest rate increases had the expected bite in household spending? The demographic component is really quite straight forward, almost one third of all homes in Australia are owned outright. So, for these residential property owners, increases in interest rates has negligible impact on their lifestyle and capacity to spend, assuming that they aren’t exposed through investment properties or other asset classes and or businesses. [TN1] With low rates of new supply in most cities and regions, rental growth has outpaced or kept pace with interest rate repayments and those persons who have held investment properties for more than three years, have also experienced significant uplift in equity, despite recent softening in some values.

Regarding timing and entry into the residential market, the lifting of interest rates actually hurts first home buyers that typically have the least amount of money and are generally not big spenders as are those who are more established in their careers and have gained significant equity over time. These buyers are usually between 15% to 23% of all new finances, with the penetration rate often depending on what cash stimulus is created to help them get into the market. So, interest rate increases do impact this percent of the market, but it is not a big part of the overall residential sector.

After a long period of minimal wage growth, the last eighteen months have seen incomes improve on the back of very tight labour market conditions. This has flowed through to every State, some benefitting more than others. Whilst interest rates have increased, so have incomes, which has been helpful in negating some of the impact of those higher borrowing costs. Had incomes remained stagnant, the RBA’s only tool of monetary policy would have been far more effective, and inflation would unlikely be where it is today.

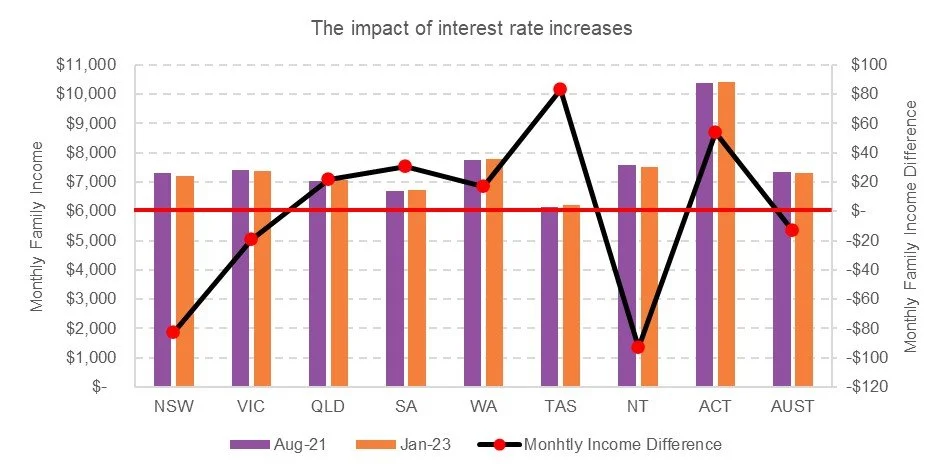

The following chart demonstrates what the monthly family income for each State was at the time of the Census less the median monthly mortgage repayment. The NPR Co then extrapolated that mortgage repayment out using the current CBA variable rate of 5.49%, assuming a loan to value ratio of between 80.01% and 90.00% on those mortgage amounts. The author would argue that this is conservative with significantly more residential borrowings below this adopted rate and therefore likely to have a lower interest rate and reduced monthly payments.

Combined with this was the escalation in wages for each family household income to get to the same point in time. Those States below the red line demonstrate a deteriorating household income position whilst those above have a slightly superior outlook, but nothing that would be considered substantive. Clearly the caveat with this graph is that it applies to the median mortgage size for each State, not new mortgages whereby those borrowers are often in a more exposed position than they were 18 months ago. The point being that there is a large proportion of Australians that are not experiencing discomfort yet with the rising interest rate environment, particularly those who own their own home outright, which is almost one in three dwellings.

Despite this, the cost of living is going up with inflation now at 7.8% for the weighted average of the eight capital cities. This is where the interest rate environment will have its greatest effect as housing prices are softening. If this was the sole goal of the RBA, then the discussion points would be around whether interest rates should decline and if so, by how much. Interestingly, that conversation might be closer than many realise.

Household savings are declining at a rate faster than any time over the past nine years which is what the RBA has been hoping to achieve. This will slow the economy as demand from consumers wanes and the brakes start to be applied by households. However, in stating that, it must also be acknowledged that household savings were at record levels which has meant households have had a greater capacity to spend. The balancing act for the RBA is to ensure that the business community is not punished as a result. Already there is a softening in the industrial sector, businesses are renting instead of buying equipment and the aggregate of business investment is at its lowest point in almost 30 years. Without doubt these are some of the most challenging economic circumstances an RBA governor has had to navigate in the past three decades. How it helps slow the economy whilst not over-correcting into a recession will be quite the juggle. Fortunately, the RBA now has some wiggle room with interest rates, should it need to move quickly.

As is usually the case, most households are very good at controlling their budgets. They are mostly highly aware of the money coming in and the money going out. It is one of the reasons that to date, interest rate increases are more a talking point than an anti-government sentiment. From the Government and RBA’s perspective though, unless geopolitical events change significantly in 2023, controlling the economy with interest rates/monetary policy alone is akin to trying to hold an eel with grease on your hands…good luck.

Matthew Gross | Director | mgross@nprco.com.au