Three Days of Market Insights

Having just completed an intense three days whereby I delivered four presentations on various markets around South East Queensland, I thought I would share with you some of the more interesting insights regarding the Gold Coast Apartment Market, Migration, Small Businesses and Interest Rates. However, before I do, it would be remiss of me not to thank the four parties that had me along to talk, Queensland Department of State Development, Villaworld Ltd, QM Properties and Lotte Engineering and Construction – a top 1 0 business group in Asia. We are very proud of the quality of our clients and enjoy being part of and contributing to, their many successes.

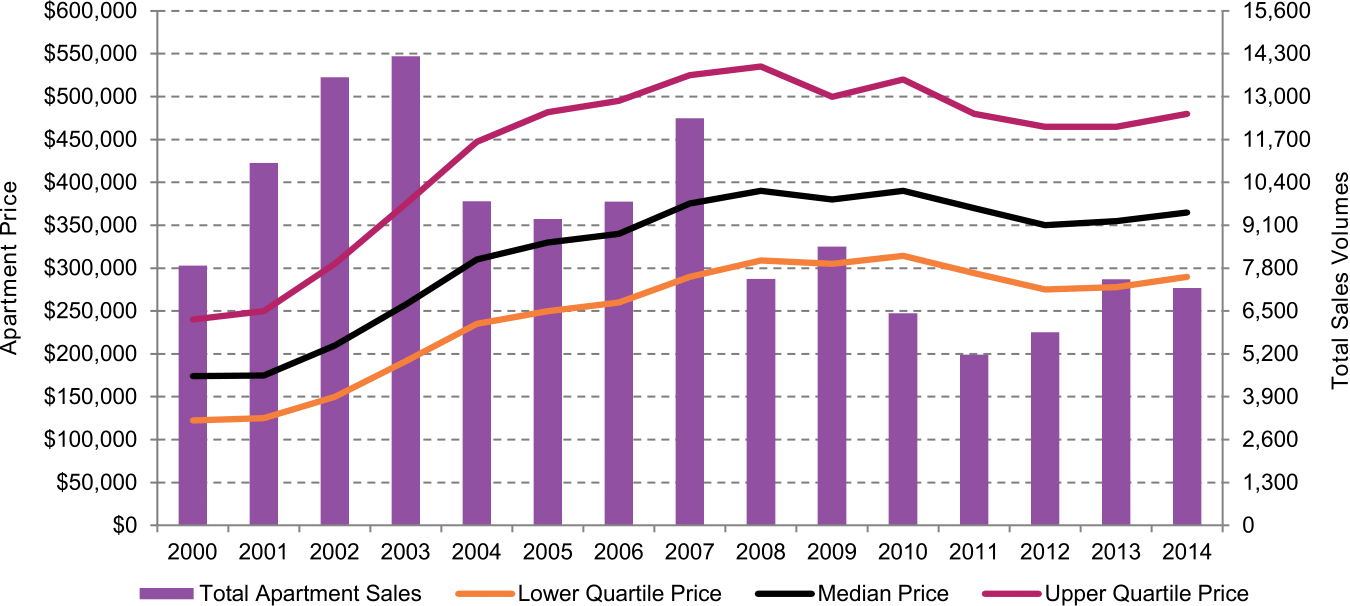

Insight 1- Gold Coast Apartments

Gold Coast LGA Apartment Sales Volumes and Median/Quartile Prices

Sales in the Gold Coast apartment market actually stalled in the second half of 201 4 in terms of total volumes. Despite the slower sales rates, the recovery in prices still gained some momentum but realistically it is not showing any of the signs of the overheating that is present in the Sydney and Melbourne markets currently. Prices are still below the peak of 2008 which suggests that the market still has many good buys remaining.

Gold Coast LGA Apartment Sales Volumes by Price Point

The broader market continues to demonstrate that over 75% of all sales occurred under the $500,000 price point. This is making it increasingly challenging for new developments as often the gap between the established market and the new market is quite substantial. This isn’t helped by the fact there are over 3,000 apartments for sale throughout the Gold Coast region.

The Gold Coast market is still chewing through much of the post GFC product and is yet to fully recover from the amount of mortgagee sales and bank work outs. Having stated that, boutique projects are selling very well. The level of international interest in the Gold Coast, both by developers and investors, suggests that there is a strong underlying confidence in the region. Projects such as Jewel demonstrate a willingness to challenge the status quo. Another example of persistence that has had to endure a tough period during the GFC is Salacia Waters. This development, which has been nominated for many UDIA awards, is now

approaching total sell out.

The 201 8 Commonwealth Games is expected to lift the local economy substantially over the ensuing three years and for a period of time thereafter. However the most recent unemployment data suggests that this is yet to fully flow through the whole region.

Insight 2- Migration

The simple reality is that population growth puts bums on seats in offices, stimulates retail and drives the consumption of housing. Interstate migration has been one of the big economic drivers for many states; however the trends are changing quite rapidly.

Interstate Migration by State 1981 - 2014

The most obvious cycle has been the level of net positive interstate migration to Western Australia that peaked during the resource boom. The June and September quarters of 201 4 actually saw WA have a net population loss, albeit minor of just negative 33 and negative 176 respectively. The last time a net migration loss occurred in WA was June 2003. This exodus lasted four years starting in June 1999. One would hope that this trend is more short lived this time around.

Queensland’s share of interstate migration increased in June and September 2014 after one of the lowest quarters on record. In March 201 0, the lowest interstate migration rate to Queensland over the past three decades was just 589, in March 201 4 the second lowest was marginally higher at just 689. There is however an expectation that interstate migration will continue to increase in QLD as the gap between the capital city house prices of Sydney and Melbourne continues to outpace Brisbane.

The real story though is the growth in interstate migration for Victoria, the self-appointed culture capital of Australia. Not only is there a cafe on every corner, Melbourne is host to many sporting events that literally stop the nation such as the Melbourne Cup, Formula One grand prix, AFL Grand Final and the Australian Open Tennis to name a few. Victoria has successfully turned around a history of net interstate migration loss to one of positive growth.

In order to achieve this significant turnaround, Melbourne and its hinterland have had millions invested in significant infrastructure. This has allowed business to increase its productivity through ring roads and the more efficient movement of freight. Not only has their town planning led the way in making this happen, it has also been acutely aware of the supply of land and the importance of ensuring strong supply for the residents. As a result, Melbourne remained highly competitive nationally for a long time. This is however starting to diminish and with it is the expectation that their interstate migration may also start to fall away.

Insight 3- Small Business

Small business remains one of the fundamentals of the Australian economy, and as a result the

property industry. For a large regional council area such as Moreton Bay, small business remains the very clear backbone of society.

Employee Numbers for Business: Moreton Bay Regional Council

With over two thirds of small businesses being represented by less than five employees, the

recent Federal budget initiative of providing $20,000 to small business will provide enormous

stimulus for this area. This will extend through the whole retail spectrum from the purchase of

computers through to small cars. Growing these grass roots businesses will provide substantial downstream benefits to the residents which will eventually flow through to greater numbers of home ownership.

Don’t underestimate the power of this one budget initiative on areas that have extraordinarily high proportions of small businesses.

Insight 4- Interest Rates

Difference Between the Cash Rate and the Standard Variable Home Loan Rate: 2000 - 2015

There is a very significant difference between the pre GFC financial era and the post GFC era. The average margin on top of the standard variable interest rate on a home loan was just 1 .8%. I f this was to exist today, the standard variable home loan would be closer to 3.8%, a substantial discount over the current interest rates.

Whilst affordability remains a significant problem in some capitals of Australia, it is reasonably fair to say that the cash rate, or interest rates in general are not to blame. Whilst it would appear that the banks probably do have the capacity to move rates down outside of the RBA, the flipside is that they are also trying to have interest rates that are available for those relying on term deposits and the like. This is clearly a challenging position for the financial institutions and one they are often not given enough credit for.

The National Property Research Company

Level 1, 307 Queen Street

BRISBANE QLD 4000

Ph 07 3229 0111